Renovation Capital Allowance Malaysia - Renovation Capital Allowance Malaysia Fees And Fox Run Facility Renovation Lessor Costs Appearing In Section 4 A Of The Sixth Amendment Shall Be Deleted In Their Entireties - Renovation capital allowance malaysia 2017.

Renovation Capital Allowance Malaysia - Renovation Capital Allowance Malaysia Fees And Fox Run Facility Renovation Lessor Costs Appearing In Section 4 A Of The Sixth Amendment Shall Be Deleted In Their Entireties - Renovation capital allowance malaysia 2017.. The section 14q deduction is applicable to qualifying capital expenses incurred on or after 16 february 2008. Initial allowance is fixed at the rate of 20% based on the original cost of the asset at the time when the capital expenditure is incurred. Accelerated capital allowance for machinery and equipment including ict equipment deduction for renovation and refurbishment expenses special reinvestment allowance small and medium enterprises (smes). In this article, seekers will share a review of 3 types of allowances with reference from the inland revenue board of malaysia (lhdn) tax ruling and how the allowances affect the tax payment. Initial allowance is granted in the year the expenditure is incurred and the asset is in use for the purpose of the business.

5 special tax deduction for renovation and refurbishment expenses a tax deduction of up to rm300,000 will be given for expenses incurred on renovation and refurbishment of business premises from 1 march 2020 to 31 december 2020. The practice note was issued on 16 march 2020 to provide guidance on the implementation of the income tax (capital International transactions until 31 december 2020. 8 oktober 2018 inland revenue board of malaysia _____ page 2 of 19 4.3 the conditions that must be fulfilled by a person to qualify for an initial allowance (ia) and an annual allowance (aa) are the same as the conditions to claim capital allowances at the normal rate under schedule Aca will be given for qualifying capital expenses incurred on machinery and equipment, including information.

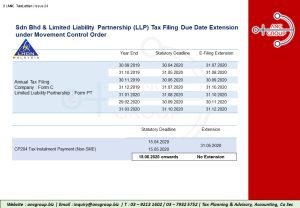

Taxletter Issue 24 Anc Group from ancgroup.biz Ken hardy and damien flanagan of our. Capital allowances consist of an initial allowance and annual allowance. Accelerated capital allowance for machinery and equipment including ict equipment deduction for renovation and refurbishment expenses special reinvestment allowance small and medium enterprises (smes). Capital allowance for leasing asset. 2) extension of accelerated capital allowance (aca) for machinery & ict equipment objective: The practice note was issued on 16 march 2020 to provide guidance on the implementation of the income tax (capital Malaysia will qualify for investment tax allowance of 100% for 5 years. In this article, seekers will share a review of 3 types of allowances with reference from the inland revenue board of malaysia (lhdn) tax ruling and how the allowances affect the tax payment.

Conditions for claiming capital allowance are :

The capital allowance rates are: Tax treatment on expenditure for repairs and renewals of assets, dated 26 november 2019, to explain the tax treatment of expenditure for the repair and renewal of an asset. The irb has published pr no. While annual allowance is a flat rate given every year based on the original cost of the asset. Capital allowances are akin to a tax deductible expense and are available in respect of qualifying capital expenditure incurred on the provision of certain assets in use for the purposes of a trade or rental business. Capital allowance is only given to business activity. The inland revenue board of malaysia (irbm) has recently issued practice note no. Chapter 2a industrial building allowances. Renovation capital allowance malaysia 2017. 3/2018 to explain the tax treatment in relation to qualifying building expenditure (qbe) and the computation of industrial building allowances (iba). Special tax deduction on costs of renovation and refurbishment Ken hardy and damien flanagan of our. Examples of assets used in a business are motor vehicles, machines, office equipment, furniture and computers.

Ken hardy and damien flanagan of our. They effectively allow a taxpayer to write off the cost of an asset over a period of time. Initial allowance is granted in the year the expenditure is incurred and the asset is in use for the purpose of the business. Foreign companies that relocate their business operations into malaysia and have made new investments in the manufacturing industry will be taxed at a rate of 0% for the following periods: Aca will be given for qualifying capital expenses incurred on machinery and equipment, including information.

The Different Types Of Capital Allowances Each Have Their Own Rules And Rates Renovation Of Business Premises In Disadvantaged Areas Pdf Free Download from docplayer.net effective for capital expenditure incurred from *1 march 2020 to 31 december 2020 A) 10 years for capital investment between rm300 million to rm500 million b) 15 years for capital investment above rm500 million The person who has the right to claim capital allowance is the person who has expended on the purchase or acquisition of the said asset. ˚is deduction shall not apply if capital allowance under schedule 2 or schedule 3 of the income 3/2018 to explain the tax treatment in relation to qualifying building expenditure (qbe) and the computation of industrial building allowances (iba). Aca will be given for qualifying capital expenses incurred on machinery and equipment, including information. Examples of assets that are used in business are motor vehicles, machines, office equipments, furniture, etc. The capital allowance rates are:

The computation of capital allowances should be consistent for each year of assessment.

Renovation capital allowance malaysia 2017. Tax treatment on expenditure for repairs and renewals of assets, dated 26 november 2019, to explain the tax treatment of expenditure for the repair and renewal of an asset. Person may submit revised capital allowances computation for all relevant years of assessment to the inland revenue board of malaysia (irbm) branch that handles his income tax file. The practice note was issued on 16 march 2020 to provide guidance on the implementation of the income tax (capital (a) 20/2010] , wherein are specified expenses incurred on the renovation and refurbishment of business premises between 10 march 2009 and 31 december 2010 be given accelerated capital allowances (aca) at the rate of 50% and qualifying expenditure for aca purposes is capped at rm100,000. Capital allowance for leasing asset. 8 oktober 2018 inland revenue board of malaysia _____ page 2 of 19 4.3 the conditions that must be fulfilled by a person to qualify for an initial allowance (ia) and an annual allowance (aa) are the same as the conditions to claim capital allowances at the normal rate under schedule To assist businesses to remain competitive and to reduce cost of doing business, it is proposed that expenses incurred on renovation and refurbishment of business premises between 10 march 2009 and 31 december 2010 be given accelerated capital allowance that can be claimed within 2 years. Examples of assets that are used in business are motor vehicles, machines, office equipments, furniture, etc. 5 special tax deduction for renovation and refurbishment expenses a tax deduction of up to rm300,000 will be given for expenses incurred on renovation and refurbishment of business premises from 1 march 2020 to 31 december 2020. Capital allowances are akin to a tax deductible expense and are available in respect of qualifying capital expenditure incurred on the provision of certain assets in use for the purposes of a trade or rental business. The section 14q deduction is applicable to qualifying capital expenses incurred on or after 16 february 2008. Question 3 5 needs help to be answeredquestion 5co chegg com.

Renovation capital allowance malaysia 2017. In this article, seekers will share a review of 3 types of allowances with reference from the inland revenue board of malaysia (lhdn) tax ruling and how the allowances affect the tax payment. Fully claimable in 2 years. Businesses that incur qualifying expenditure on renovation and refurbishment of its business premises from 1 march 2020 to 31 december 2020 shall be given tax deduction up to rm300,000. Capital allowances consist of an initial allowance and annual allowance.

Capital Allowance Deductions 1 Capital Allowance Deductions Scd 2 6 1 Introduction Capital Allowances Reduce The Taxable Income In Accordance Course Hero from www.coursehero.com The section 14q deduction is applicable to qualifying capital expenses incurred on or after 16 february 2008. To incentivise businesses to invest in 2020, the annual allowance is increased to 40%. Ken hardy and damien flanagan of our. Fully claimable in 2 years. 2) extension of accelerated capital allowance (aca) for machinery & ict equipment objective: Mahathir mohamad on 27 february 2020. The rules provide that in ascertaining the adjusted income of a person from its business for a ya, there shall be allowed a deduction, capped at rm300,000, for the costs of renovation and refurbishment of a business premise incurred by the person from 1 march 2020 until 31 december 2021, and used for the purpose of its business. Malaysia will qualify for investment tax allowance of 100% for 5 years.

The practice note was issued on 16 march 2020 to provide guidance on the implementation of the income tax (capital

To assist businesses to remain competitive and to reduce cost of doing business, it is proposed that expenses incurred on renovation and refurbishment of business premises between 10 march 2009 and 31 december 2010 be given accelerated capital allowance that can be claimed within 2 years. The computation of capital allowances should be consistent for each year of assessment. Business rent rent dividend interest malaysia malaysia australia malaysia china rm rm rm rm rm gross income 600 000 72 000 40 000 20 000 course hero. Capital allowances consist of an initial allowance and annual allowance. 3/2018 to explain the tax treatment in relation to qualifying building expenditure (qbe) and the computation of industrial building allowances (iba). effective for capital expenditure incurred from *1 march 2020 to 31 december 2020 To incentivise businesses to invest in 2020, the annual allowance is increased to 40%. The government has initially introduced special tax deduction on cost of renovation incurred from 1 march to 31 december 2020 in the first economic stimulus package announced by our former prime minister, tun dr. Initial allowance is fixed at the rate of 20% based on the original cost of the asset at the time when the capital expenditure is incurred. 5 special tax deduction for renovation and refurbishment expenses a tax deduction of up to rm300,000 will be given for expenses incurred on renovation and refurbishment of business premises from 1 march 2020 to 31 december 2020. Question 3 5 needs help to be answeredquestion 5co chegg com. It has now been extended to 31 december 2021. ˚is deduction shall not apply if capital allowance under schedule 2 or schedule 3 of the income

Related : Renovation Capital Allowance Malaysia - Renovation Capital Allowance Malaysia Fees And Fox Run Facility Renovation Lessor Costs Appearing In Section 4 A Of The Sixth Amendment Shall Be Deleted In Their Entireties - Renovation capital allowance malaysia 2017..